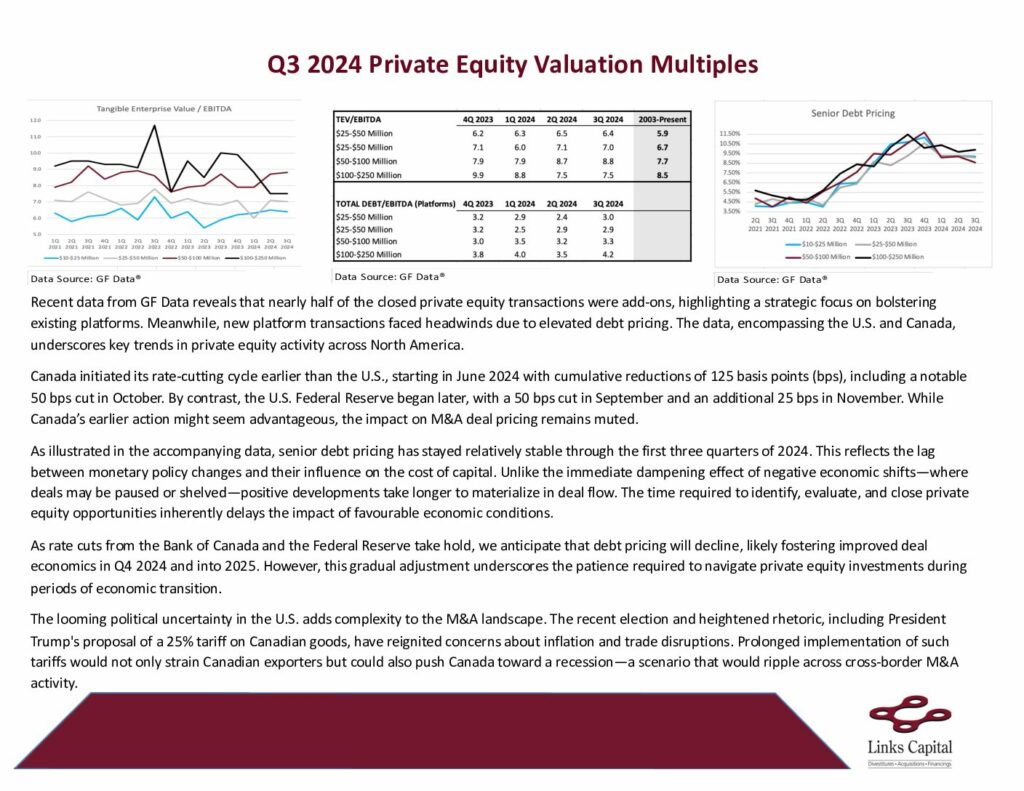

Recent data from GF Data reveals that nearly half of the closed private equity transactions were add-ons, highlighting a strategic focus on bolstering existing platforms. Meanwhile, new platform transactions faced headwinds due to elevated debt pricing. The data, encompassing the U.S. and Canada, underscores key trends in private equity activity across North America.

Canada initiated its rate-cutting cycle earlier than the U.S., starting in June 2024 with cumulative reductions of 125 basis points (bps), including a notable 50 bps cut in October. By contrast, the U.S. Federal Reserve began later, with a 50 bps cut in September and an additional 25 bps in November. While Canada’s earlier action might seem advantageous, the impact on M&A deal pricing remains muted.

As illustrated in the accompanying data, senior debt pricing has stayed relatively stable through the first three quarters of 2024. This reflects the lag between monetary policy changes and their influence on the cost of capital. Unlike the immediate dampening effect of negative economic shifts—where deals may be paused or shelved—positive developments take longer to materialize in deal flow. The time required to identify, evaluate, and close private equity opportunities inherently delays the impact of favourable economic conditions.