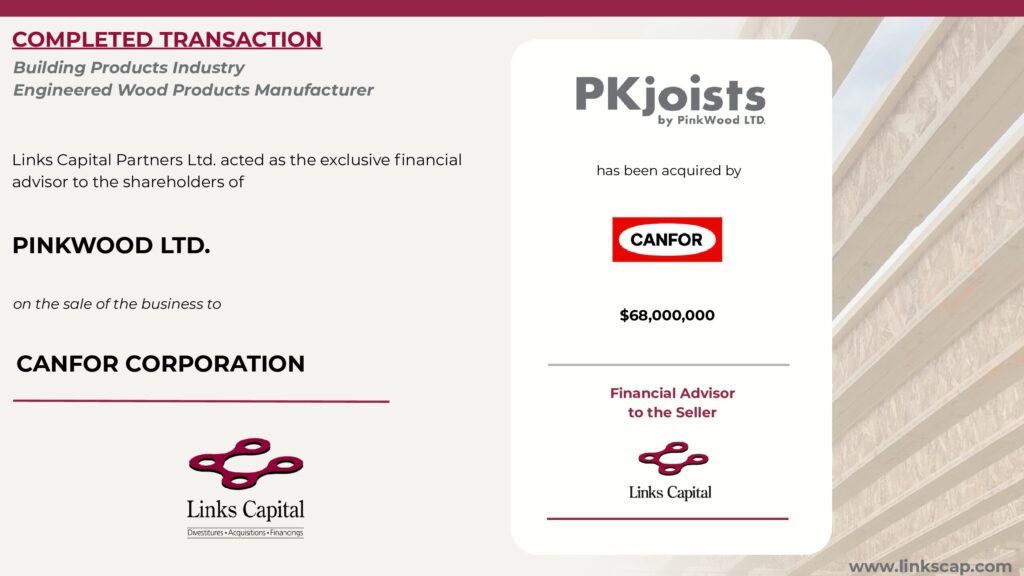

Pinkwood acquired by Canfor

Links Capital Partners Ltd. is pleased to announce that it acted as the exclusive financial advisor to the shareholders of PinkWood Ltd. on its $68,000,000 sale to Canfor Corporation (TSX: CFP).

The relationship with the principal shareholder began more than 20 years ago. Over that time, Links Capital advised on the sale of his previous business, helped secure financing to support PinkWood’s growth and ultimately advised the shareholders on the sale of the company to Canfor.

This transaction reflects the value of relationships developed over many years. Links Capital is grateful for the trust placed in the firm over the past two decades and for the opportunity to be part of PinkWood’s journey from its early years through to this successful transaction.

Congratulations to the shareholders, management team and employees of PinkWood on building an outstanding company, and to Canfor on this acquisition. Thank you for the confidence placed in Links Capital and for the opportunity to be part of this journey

Pinkwood acquired by Canfor Read More »